![]()

![]()

SS Age

70

62

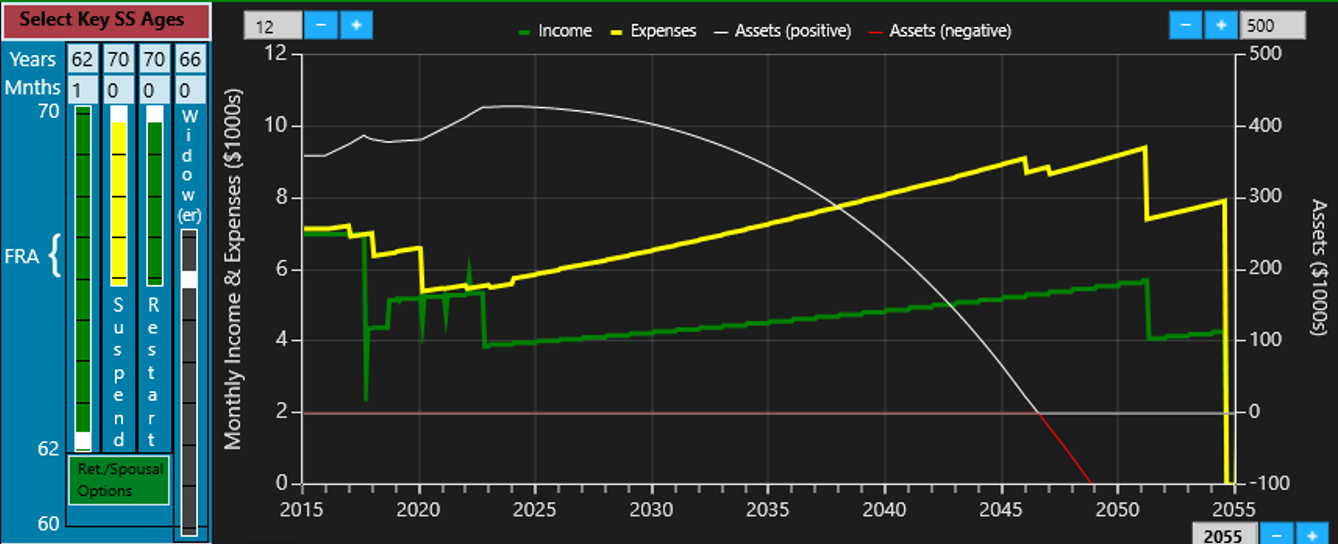

Social Security & Retirement Financial Modeling is a Windows app that has been developed to help those approaching retirement, or in retirement, get an assessment of what their financial future may hold. SS&R can help answer such questions as:

Answers to the above questions are always dependent on the particulars of our situation. Primary among those particulars are: Work status, anticipated longevity, marriage situation, retirement and non-retirement savings, expenses, pensions, and potential Social Security benefits. Given the difficulty of comprehending the interactions between income, savings, taxes, and Social Security benefits in even the short term, and given that retirement decisions can have a financial impact two, three, or even four decades down the road, help is needed to peer into the foggy future. Wouldn't you agree that having a means to combine the particulars, handle the interactions, and project the consequences of retirement decisions into and through our retirement years is worth more than a cup of coffee?

Additional information about SS&R is presented below, and further details are available in the pdf User's Guide (accessable at the top of the page). The SS&R's guide will step you through four example situations: Mary Lamb; Jack and Jill Water; Mr. and Mrs. L. J. Horner; and Mr. and Mrs. O. K. Cole. The more time you spend evaluating, the more you will see the amazing value that SS&R provides!

If SS&R is going to comprehend the particulars of a person's, or couple's, financial situation, that means the user must provide* the pertinent data. What is required?

What elements of Social Security and the IRS does SS&R incorporate? For Social Security:

For the IRS:

What limitations and assumptions exist in SS&R relative to Social Security and the IRS? SS&R does not deal with Social Security benefits for children or the disabled, does not deal with the Government Pension Offset for workers who have, obviously, a government pension, and does not accommodate the Social Security “Windexing” provisions that may be beneficial to widows/widowers whose spouses died prior to age 62.

Relative to the IRS, calculations comprehend single or married status, but not head of household. Standard deductions are assumed, including, when appropriate, the additional deduction available to those over 65. It follows that itemized deductions are not accommodated, and neither are deductions for contributions to retirement accounts. Since SS&R is making estimates out into future years, it is assumed the structure of federal taxes remains fixed, but tax brackets are indexed to the projected cost-of-living changes. Required Minimum Distributions from tax-deferred retirement accounts are calculated, in all cases, using the IRS’s “Uniform Lifetime Table.” (If the account owner’s spouse is more than 10 years younger than the account owner, the less demanding “Joint Life and Last Survivor Expectancy Table” may be more advantageous.)

It should also be mentioned that capital gains on non-retirement assets are assumed to be realized each and every year. As required by the IRS, capital losses in excess of $3000 are carried over to the following year. SS&R, with default settings, assumes gains in non-retirement assets are split evenly between long-term capital gains and ordinary income items (e.g., short-term capital gains, CD interest, and non-qualified dividends). The user, however, has the option of specifying a different ratio if their non-retirement account investments are better represented by something other than a 50:50 split.

Because SS&R includes all the taxes typically encountered by Joe Taxpayer, but conservatively assumes standard deductions, tax estimates should tend to miss on the high side. Consequently, the calculation of total assets over time should tend to miss on the low side for those who benefit by itemizing deductions.

SS&R, utilizing 2022 Social Security and US federal tax parameters, 2020 Social Security actuarial information, inputs/assumptions concerning future market performance and cost-of-living changes, along with inputs that describe a person's or couple's current financial situation, strives to project that situation out into the future. The world, however, is not orderly. As the bumper sticker says, 'Shit happens.' Rules change, situations change, and it's even possible, truth-be-told, that coding errors exist that impact the outputs of SS&R. Thus, SS&R is, and should be viewed as, a well-intentioned assistant, not a source of "Gospel truth."

*SS&R is not set-up to access the internet. Thus, for example, your Social Security PIA must be obtained independently and manually entered into SS&R. It should be noted, however, there is nothing to prevent a user from saving/loading an SS&R data file to/from an internet accessed storage location (e.g.,Google Drive).